Weekly Market Commentary – 7/16/2021

-Darren Leavitt, CFA

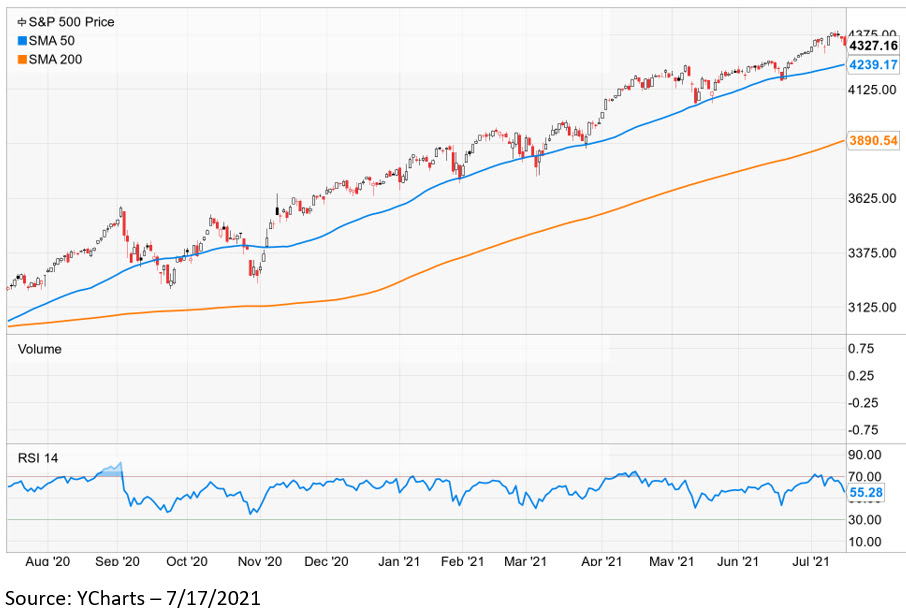

Despite hitting another set of all-time highs, US financial markets ended the week lower. 2nd quarter earnings kicked off with better than expected results from the financials; however, banks shares generally sold off in the wake of the announcements. Fed Chairman Jerome Powell was on the Hill for his semiannual testimony on monetary policy. The Fed Chair reiterated that the Fed would continue to be accommodative for quite some time while acknowledging the recent increases in inflation. Economic data was mixed for the week but headlined by the Consumer Price Index (CPI) and the Producer Price Index (PPI), which both came in hotter than expected.

The S&P 500 lost 1% for the week, the Dow gave back 0.5%, the NASDAQ declined 1.9%, and the Russell plunged 5.1%. The most recent rotational trade between Growth and Cyclicals changed to selling Growth and Cyclicals and buying defensive sectors. Utilities, Real Estate, and Consumer Staples held up well while Energy, Financials, Materials, and Semiconductors sold off. The Semiconductor sector had a tough week on the back of disappointing earnings from Taiwan Semiconductor (TSM). The yield curve flattened as the 2-year note yield increased two basis points to 0.23%, and the 10-year yield fell six basis points to close at 1.30%. The 2-10 spread declined by eight basis points to 107. Oil prices fell on news that OPEC had reached a supply agreement. WTI prices fell 3.75% or $2.80 to close at $71.76 a barrel. Gold prices increased by $4.40, closing at 1815.10 an Oz.

The much anticipated CPI print was stronger than expected, coming in at 0.9% versus expectations of 0.7%. The reading showed price increases across each category. Similarly, the Producers Price Index was also hotter than expected. The headline number came in at 1%, while the consensus estimate was 0.6%- annualized PPI is running at 7.3%. June Retail sales were much better than expected, coming in at 0.6 versus the forecast of -0.6%. Initial Jobless claims came in at 360K, and Continuing Claims showed progress at 3.241 million. Preliminary July U of M consumer sentiment was noticeably weaker at 80.6 from June’s final reading of 85.5. Interestingly, the weakness was attributed to fears about increased inflation.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.