Weekly Market Commentary – 10/22/2021

-Darren Leavitt, CFA

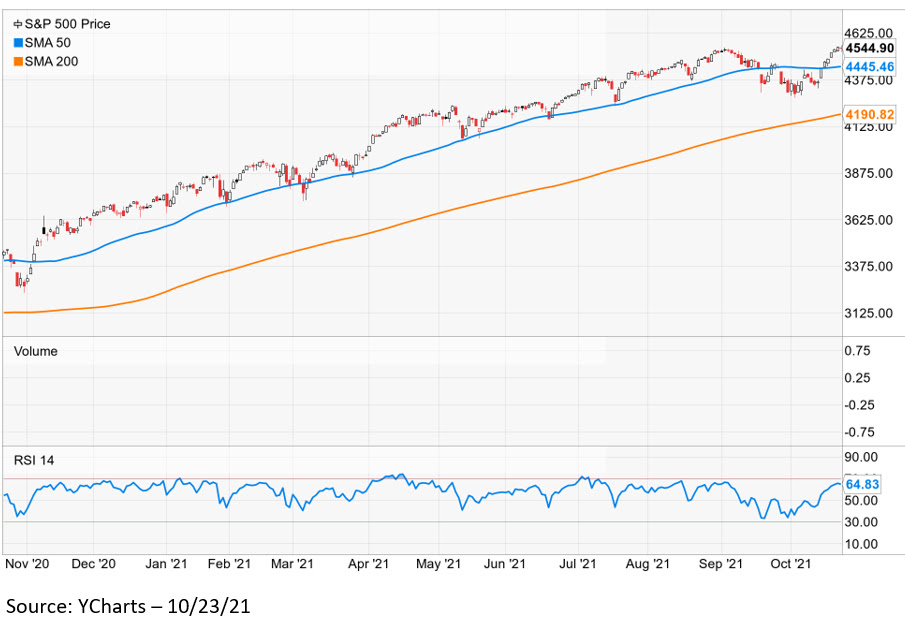

US financial markets rallied throughout most of the week, with the S&P 500 touching a new intraday high and the Dow closing at a new all-time high. Corporate earnings dominated the headlines and were, for the most part, better than expected. So far, 84% of the companies that have reported have produced better than expected results. However, this week, several companies took down forward guidance related to supply chain constraints. Proctor and Gamble highlighted the price increases of raw materials, which reduced their margins. Intel had problems sourcing materials to build its Semiconductors. Beyond Meat missed the mark and noted that the restaurant business has not fully recovered to pre-pandemic levels. Snap Chat’s earnings were also a big disappointment. The company took down guidance for the coming quarters based upon changes to Apple’s privacy policies that will likely impact their advertising efforts. The announcement took Facebook, and Google shares lower and affected the overall communications services sector. On the other hand, American Express had a great quarter and highlighted some encouraging spending trends that took hold over the 3rd quarter. Economic data for the week was mixed but remained encouraging on the labor front.

The S&P 500 gained 1.6% for the week, the Dow added 1.1%, the NASDAQ increased by 1.3%, and the Russell 2000 rose by 1.1%. Fears that the Federal Reserve would raise its policy rate sooner than expected hit the US Treasury market. The 2-year note yield increased seven basis points for the week to close at 0.47%. The 10-year yield increased eight basis points to 1.66%. Fed Chairman Powell spoke on Friday and again acknowledged that the Fed would begin tapering its asset purchase program in the coming month and would likely eliminate the program by the middle of 2022. The Fed Chair did say the Fed would be cautious with its policy rate and still expects that inflation will subside over the next several months as supply chains normalize. Oil prices continued their ascent. WTI prices increased by $1.51 or 1.8% on the week to close at $83.77 a barrel. Gold prices increased by $28.2, closing at $1796.30 an Oz.

High-frequency labor data continued to trend in the right direction. Initial Claims for the week came in at 290k better than the 303k that had been expected, and continuing claims fell to 2.481million from the prior week’s reading of 2.603 million. Housing data was a bit of a disappointment and may reflect the higher input costs associated with building. Housing starts came in at 1555K versus expectations of 1635k, and Building Permits came in at 1589k compared to the consensus estimate of 1690k. Preliminary IHS Markit Manufacturing and Services showed that both sides of the economy continue to be expansionary. The Manufacturing data came in at 59.2 compared to the prior reading of 60.7, while Services came in at 58.2 better than the previous reading of 54.9.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.